In the last post Annuity via SRS increases the monthly payouts I had analysed how SRS (Supplementary Retirement Scheme) benefits Singapore Citizens and PR’s (Permanent Residents). In this post we will determine at what level the scheme becomes beneficial for foreigners, i.e. those working in Singapore on Employment Pass or have setup businesses.

Before jumping into data driven analysis let me list out the small difference in the scheme for the two groups.

- A foreigner can withdraw the whole amount in SRS account, without paying the 5% penalty, after 10 years of making the first contribution

- Only 50% of the withdrawn amount is taxed when withdrawn after 10 years

- The tax is determined by adding the taxable amount to the income of the year to determine tax liability

- If you are not a tax resident in the year of withdrawal, then a flat rate of 22% or tax resident rate whichever is higher is used to determine the tax liability (SRS income gets added under Other Income for tax purposes)

What this means is that if you started contributing on say 1 Jan 2010, then you can withdraw the accumulated amount in SRS on or after 2 Jan 2020 without paying the 5% penalty (this option is only available to foreigners so if you are planning to become a PR then do consider this option, specially if you need that lumpsum amount for a better investment opportunity or buying a house).

Next to remember is marginal rate of tax – say your income in the year of withdrawal is SGD 120,000 and you are in 11.5% tax bracket, then the SRS withdrawal will get added to 120,000 and attract tax rate of higher slabs.

If you are planning to return to your country of origin for good, then leaving Singapore in the second half of the year gives you slightly favorable tax treatment as you remain tax resident for the year and don’t get taxed at a flat non resident rate. If your destination is India, then a return between 1 Oct to 31 Dec is the sweet spot and gives you maximum tax benefits in both countries.

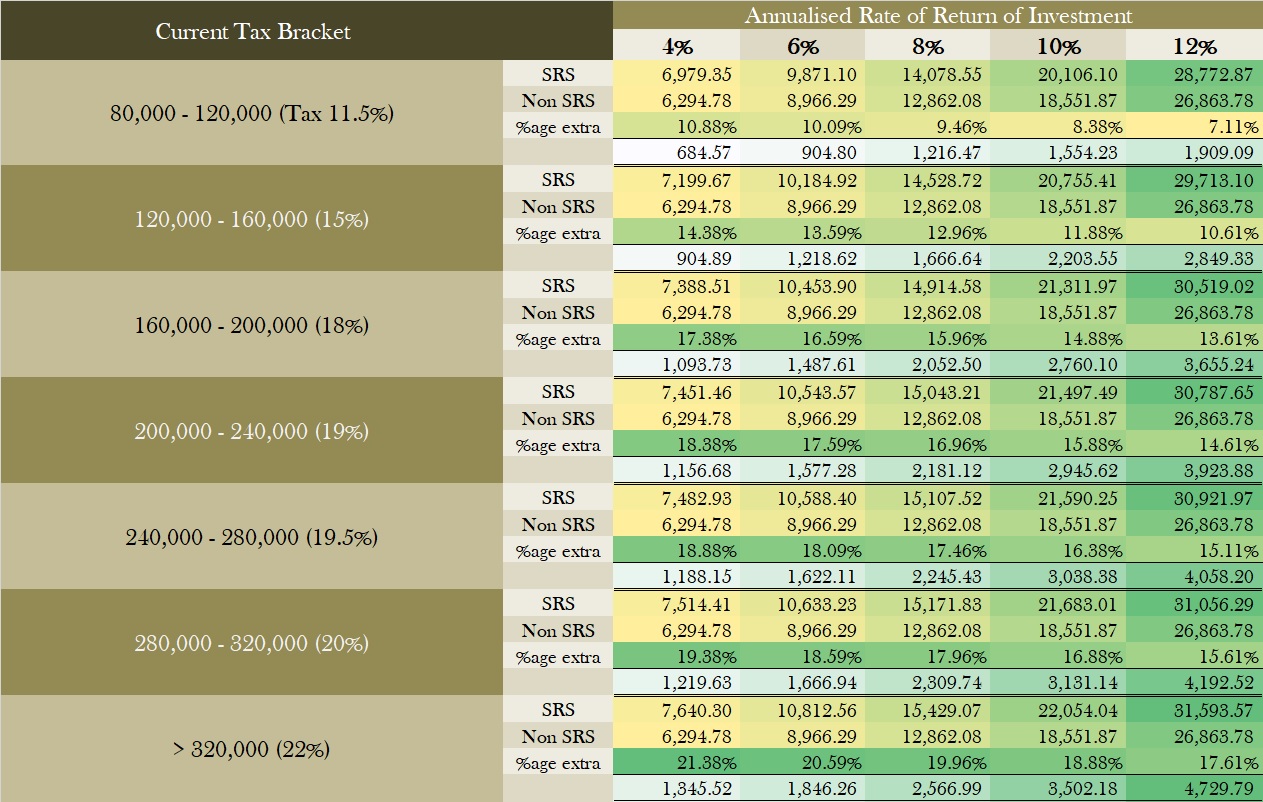

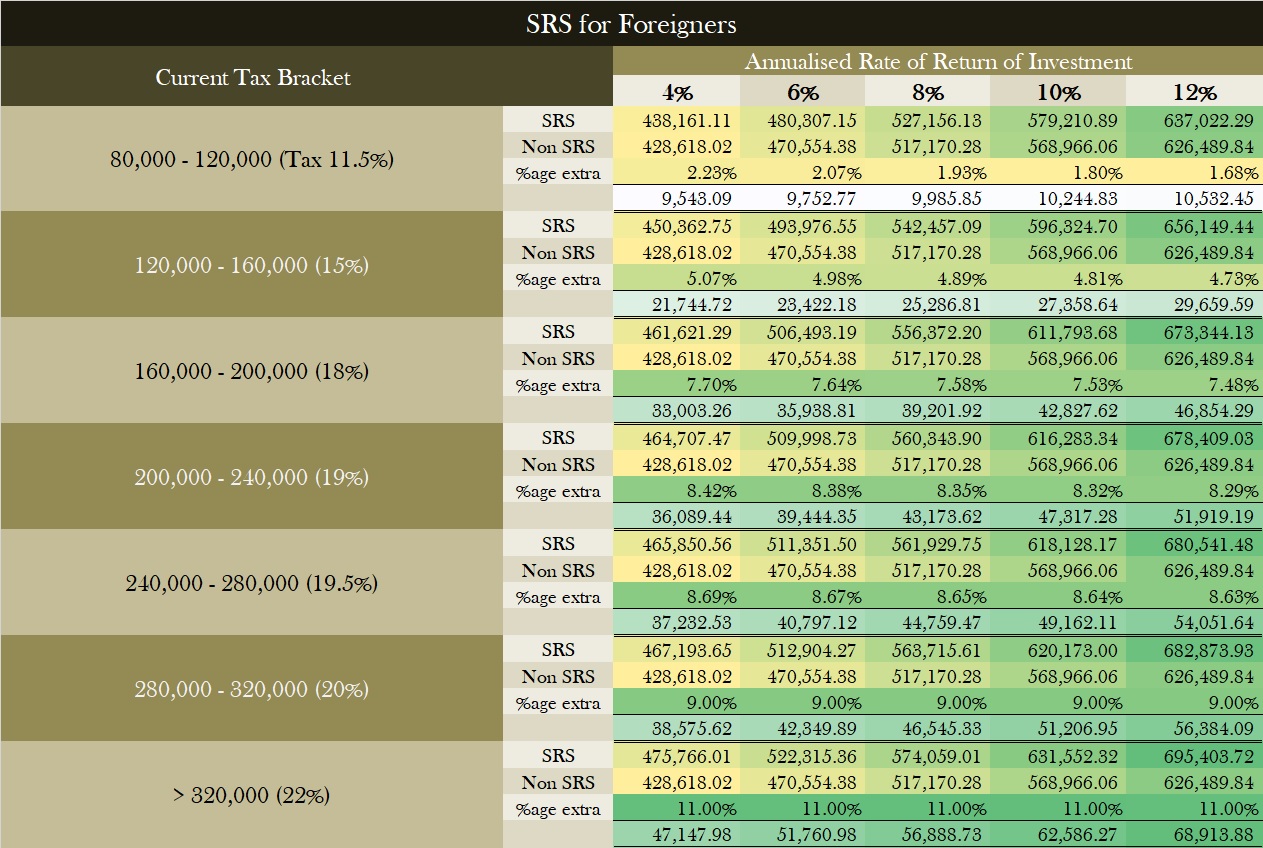

Is SRS really beneficial for foreigners?

To determine this, running calculations for various income levels, tax brackets and varying rates of return was the best bet. It took a while to not just run the algorithm but also verify for accuracy so that the readers get a nice matrix to use as for reference.

This time around I took a contribution period of 10 years and full contribution amount of 35,700 to SRS with the pre-requisite that the person also invests the tax saved on account of SRS in similar return generating portfolio outside of SRS. What this means is that if you contributed 35,700 and are in 11.5% tax bracket, you invest the tax saving of $4105 in similar portfolio as SRS and not spend it.

Data shows that if you are earning less than 120,000 per year the benefit of contributing to SRS are negligible though SRS does become beneficial as your earnings increase and tax rate increases. The key for me though is that SRS contributions don’t leave you worse off in any scenario.

You can decide to contribute to SRS or not based on your personal circumstances and the benefits matrix tabulated above. However, if your employer provides for CPF equivalent contribution only via SRS and to get that benefit you have to contribute to SRS then contributing to SRS is a no brainer. Foregoing that income just because you don’t want to contribute to SRS is an outright loss.

I would strongly recommend that everyone opens an SRS account the year they come to Singapore and make a small contribution to lock in your 10 year period and also the maturity age. Even if they don’t contribute in subsequent years there is nothing really to loose.

When should I withdraw from SRS?

If your SRS account is less than 10 years old then waiting for the remaining years can be beneficial. On withdrawal before completing 10 years, the whole amount gets added to your income and you also pay 5% penalty. So avoid doing this as much as possible.

If you decide to wait for SRS to mature (either 10 years target or full maturity at the age of 62) and are no longer Singapore tax resident then do think about how your country of residence treats dividends and capital gains that accumulate in SRS account during this period.

As an example, for Indian tax residents, all foreign income must be declared while filing taxes and taxes paid on, this means that any dividends or interest that you receive on your SRS account while waiting to withdraw must be detailed in your Indian tax returns. Any gains made due to sale of investments (e.g. Unit trusts, stocks) will be liable for capital gain taxes of that year. Failure to disclose may result in the entire amount being taxed when remitted back to India.

There are provisions to claim double taxation relief which may or may not apply based on each person’s circumstamces, if in doubt, get a qualified tax professional to prepare your tax return.

As with citizens and PR’s, contributing to SRS once in 15% bracket or higher is definitely worth it. Feel free to post in comments if you think there are situations where SRS does not make sense, we can analyse and debate the scenarios.