Let me forewarn, this post is heavy on numbers but I have tried to simplify the results as much as possible so you don’t have to do the heavy crunching. However, if you love the language of numbers (like I do) then happy to discuss variations in comments.

I had always wondered, is SRS actually beneficial in the long run and how do the returns stack up when compared to investing the amount directly and not contributing to SRS thereby foregoing the tax benefits.

SRS withdrawals attract tax on 50% of the withdrawals after the maturity date which means that the accumulated capital gains and dividends in your account do get taxed. On the flip side, the capital gains and dividends outside of SRS account or through money invested in CPF are tax free. So the big question I had in my mind was – do I end up worse off if I put money in SRS by virtue of having to pay tax on half of my gains on withdrawal.

Anlysing various scenarios and coming to a conclusion was my best bet.

Methodology

For calculations, I took a contribution period of 25 years – from the age of 37 to 62, assumption being that by then the salary / earnings of an individual have grown enough to be able to put aside some extra money towards savings. Not many people would have enough surplus to contribute towards the SRS in the initial years of employment.

It is assumed that the person contributes 15,300 per year for the calculation period and is also able to invest the tax saved on account of SRS in similar return generating portfolio outside of SRS to maximise returns. What this means is that if you contributed 15,300 and are in 11.5% tax bracket, you invest the tax saving of $1759 in similar portfolio as SRS and not spend it all.

Last assumption was that on reaching withdrawal age, you have no other taxable income and the tax rates remain at the same levels in future (this is a big assumption but for comparison I did not have any other choice)

Results

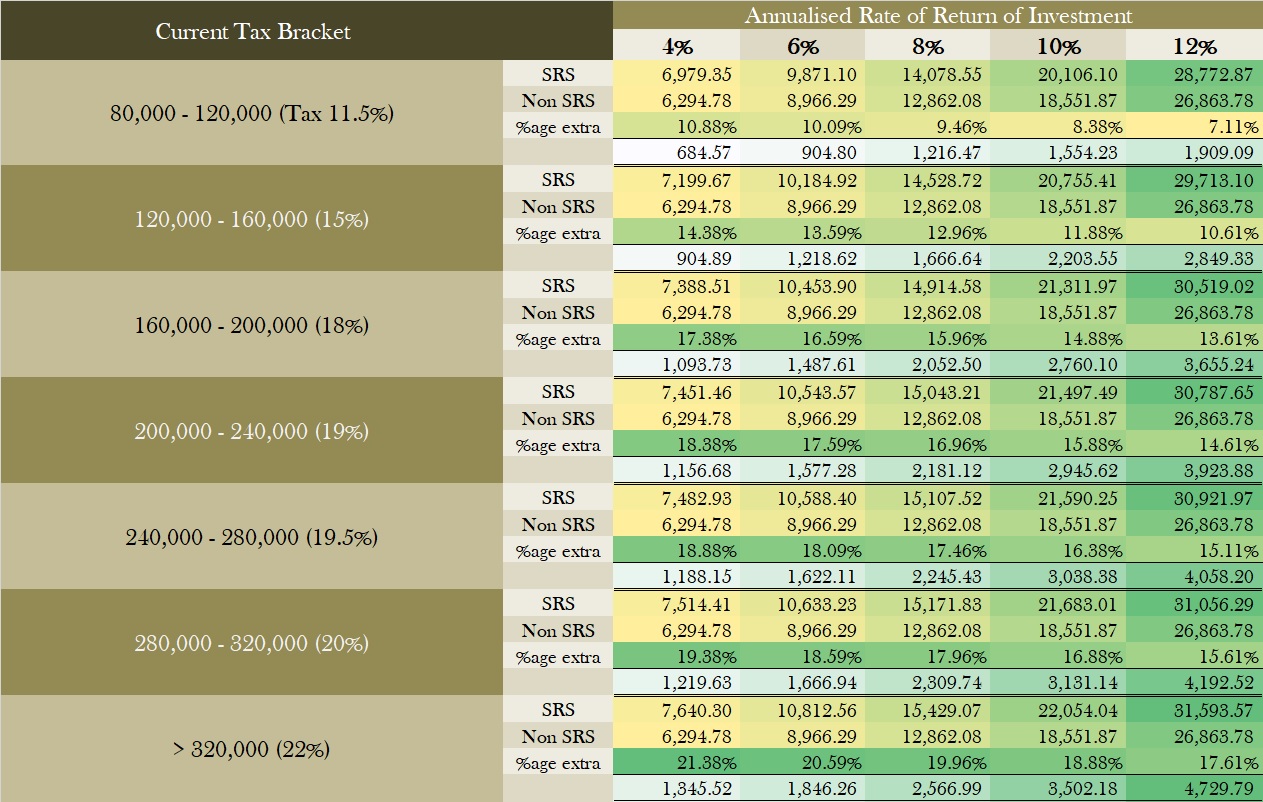

The results were a relief, to say the least. Even though I would end up paying tax on half of my gains the numbers indicated overall gains by contributing to SRS. The most interesting observation was that at around 4% yearly return, contribution in SRS would generate an additional payout close to your tax bracket.

So if you are in 11.5% tax bracket and invested the money through your SRS account, then that contribution yields additional 10.88 % as compared to having invested the same amount independently. The difference comes due to the tax savings.

The percentage gains reduce as your return on investments increases (see table below) but for you to be worse off by investing through SRS you would need a portfolio that can compound at a rate of 22% or more which is a rare feat to achieve.

Looking at the table its evident that the higher the tax bracket one is in, higher are the gains by contributing to SRS. I would personally not contribute full amount to SRS if you are in a tax bracket lower than 11.5%. The gains are marginal and having money locked in for long makes it un-attractive (atleast to me) though do open an SRS account as soon as possible even if you are going to contribute 100$ once to lock in the maturity age.

Risks

SRS accounts have their drawbacks and quirks. The money is locked till you are 62 and any withdrawals before that attract penalty and the whole amount gets added to your income in the year of withdrawal.

The returns will also go down if the tax rates by the time one retires move up and if financial standing of Singapore changes.

The calculations get trickier if done for a foreigner who wants to withdraw the money when leaving the country and I will try and tackle that in a subsequent post