As an NRI, you would have wondered many times, what parts of your Indian Income are taxable and what are not and trust me you are not alone.

Under the Indian Income tax act, the tax rates, deductions from income, exemptions from taxation all change depending on the nature of income and residential status of the individual. With the ever changing tax provisions, even if you searched online the chances of finding the information you are looking for would not be easy and filtering out the tax provisions that are applicable to an NRI is even more difficult.

Not being able to find consolidated tax provisions on common investments used by NRI’s I decided to compile the information myself and hope that fellow NRI’s will find it useful.

NRI’s mostly invest in Fixed Deposits, Bonds, Mutual Funds, Stock and Property which would generally give rise to income under Capital Gains or Other Income (Bank Interest or Dividends) under the Indian Tax laws.

I have tabulated the provisions that an NRI should be aware of for FY 2017-2018 (click on table to open in new window)

One of the most interesting things to note is that the basic tax free exemption is not available to an NRI on Equity Investments. What that means is that if an NRI gained 2,50,000 Rupee by investing in stock market the whole 2,50,000 Rupee is taxable. If these gains are long term (asset held for more than 1 year) then there is no tax liability but for short term gains the tax rate is @ 15%. So an NRI would pay Rs.37,500 in taxes, the income would not attract any tax in hands of a resident Indian.

Another interesting fact to note is that the gains on redemption of Sovereign Gold Bonds are not chargeable to tax if held till maturity.

With difference in tax rules being different in different countries an investor should consider the tax domicile of the investment to maximise returns. In Singapore and Hong Kong the Capital gains, Bank Interest and Dividends are not taxable, however in USA and UK these income are taxable.

For example if an NRI bought a mutual fund in India that returned 20% over a period of 6 months then his gains would be taxed at a flat rate of 15% resulting in a post tax return of 17%. Buying this same fund in Singapore would have been as the gains are tax free and the investor pays no tax.

Similarly for bonds the interest is taxable in India and taxed at the marginal rate based on your income bracket but tax free in Singapore and Hong Kong.

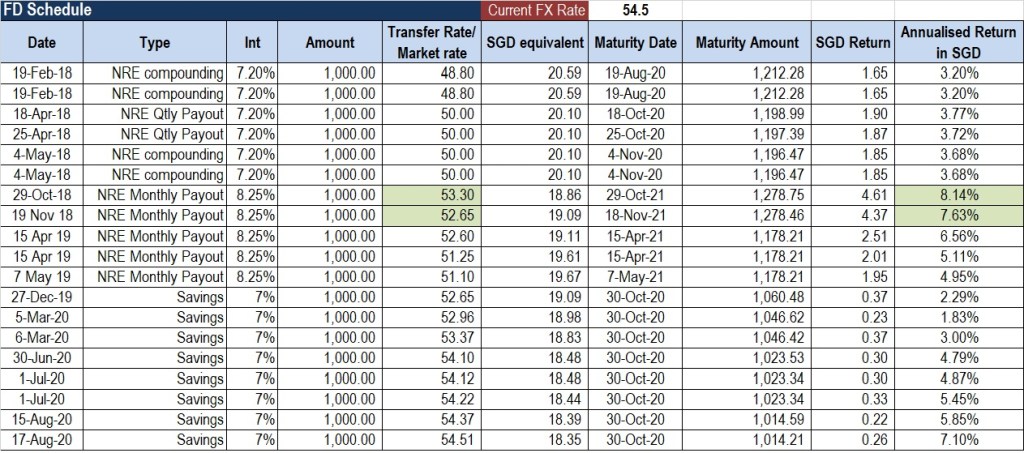

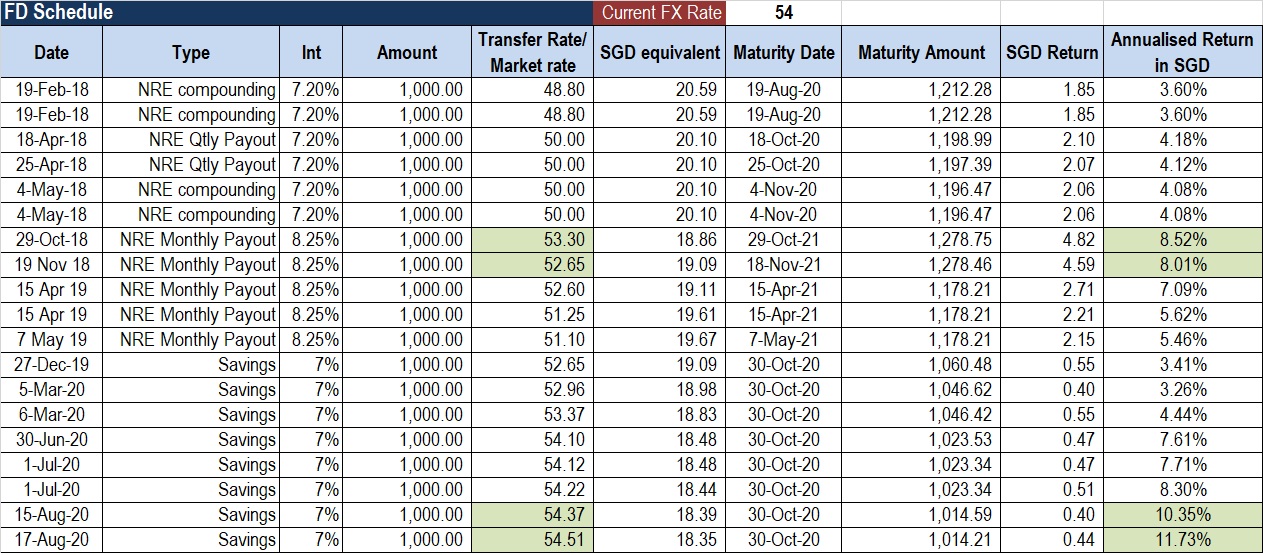

E.g . An NRI whose total income is over Rs. 10 lac (30% tax bracket) buys a bond that pays 9% interest p.a. The post tax yield of this investment would be 6.3% . Add to it the cost of transferring funds to India of around 0.8%, the yield drops to 5.5%. If the plan is to remit the money back to Singapore on maturity, which will cost another 1%, the investment would yield 4.5% only.

These are just 2 examples to get you thinking. There innumerable scenarios that I can come up with based on different countries of residence and each individuals tax profile. All I would like to highlight is that an investor should not underestimate the impact of taxation and ancillary costs while making investment decisions and look at all aspects before making an investment decision.

Watch out for an investment comparison tool that I am working and will post it here very soon. Till then keep reading and sharing.