While it maybe difficult to time any market timing does play an important role and could be the difference between ordinary and stellar returns.

Timing of transferring money to India and investing in NRE Deposits or any other investment vehicle could also mean the difference between a 3% compounded return vs returns of 7% or more.

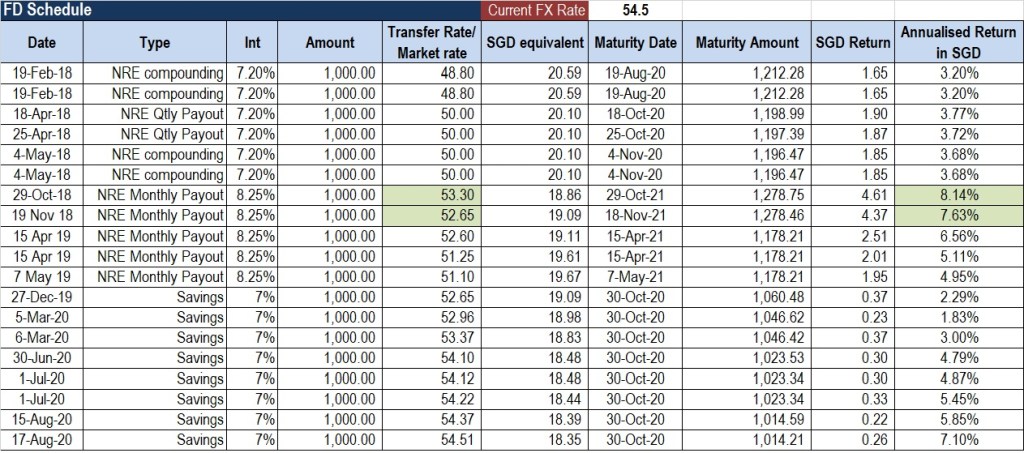

To illustrate this, I took the money transfers I have done over the past few years and tabulated a return table. I factored in cost of transferring funds i.e. nett money received in India and also the cost of repatriating the money back on maturity and using today’s exchange rate

As you would see the return ranges from anywhere between 3% to 8%, even for transfers which were done not too far apart.

The best returns were achieved when the SGD INR rate was well beyond what fundamentals commanded – like in 2018 the fair value of SGD INR was around 52 and a transfer made at 53.3 generated a superior return

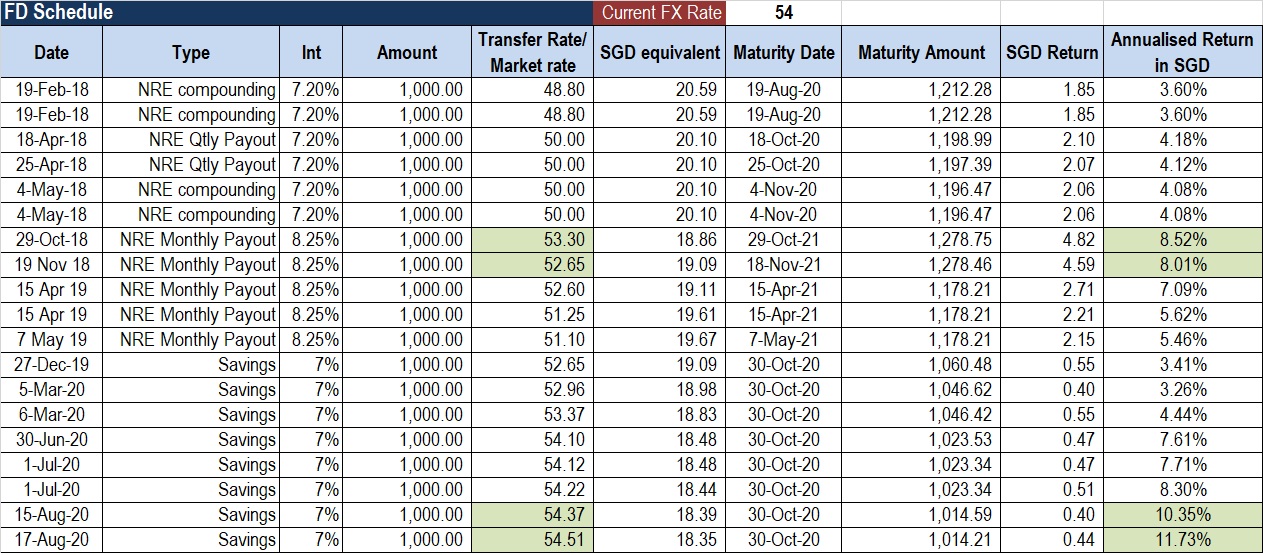

If the exchange rate moved favorably or stayed flat the returns went up. Return matrix using exchange rate of 54

Based on long term interest rate parity, i believe 54.5 -55 is fair value for SGD INR towards the end of 2020. So if the pair crosses 55 and banks are still offering 6% or more NRE FD’s then it would be a good investment to consider.

I would be keen to hear what your experience with generating stable returns in India has been

Hi Aditya

Anytime if rate is above 54.5 then transfer and park it in NRE FD”s seems best bet until COVID comes to an end. Plz suggest if you see any better options also.

Thank you for your time

LikeLike

Hi Reddy

I am expecting the rate to cross 55 between today and Diwali depending upon the outcome of the US elections.

NRE Fd is good if you can a targeted exchange rate. Keeping money in Cpf SA is a good option as well if you are a citizen or PR. I would even recommend top-ups to SA.

There are some good non Cpf options in Singapore I will be writing about them soon. Keep checking the blog 🙂

LikeLike

I have a updated post with latest NRE Fd rates, have a look

LikeLike

I just transferred another 5k via BigPay, I got a rate of 54.24

LikeLike

I think we might get 55.5 next week

LikeLiked by 1 person

Hi Nitin

TransferWise rate is 54.45. You are the master in exploring options. I used SCB from your suggestion and got good rate 2 months ago. Plz post if you find any better transfer options and investment options in India – NRE or SG. Equties seems too risky and time consuming.

LikeLiked by 1 person

I transferred again 5k through Bigpay and got a net rate of 54.37 after fees and spread. But I will get 1.5% rebate from Amex card for this. So it will turn out to be above 55 🙂

LikeLike

Isint the limit 5k per month?

LikeLike

There is a daily limit of 5k and a monthly limit of 10k. This is for both Grab and BigPay. So they are both aligned. In addition, Grab has an annual limit of 30k. But this gets reset end of calendar year.

LikeLike

Good analysis.

LikeLike

Hi Aditya,

Which bank was paying 8.25% in 2018 and 2019 ? Now, I don’t see any bank even paying beyond 6%.

Thanks Sridhar

LikeLike

Hi Sridhar, I locked 8.25% with IDFC First bank in 2018. Their savings account still gives 7%. If you want to open an account let me know and I will be happy to refer

LikeLiked by 1 person

Just curious what percent of your networth would you keep in one bank like IDFC first?

LikeLike

I would not go beyond 5%. Technically all banks are risky beyond 5 lakh rupees. While selecting a bank I would not touch a co-operative bank, then exclude small time private players, then exclude big private players who have grown too fast, then look at Balance sheet and management and even exclude foreign banks like Deutsche and HSBC whose parent entities are struggling. If any foreign bank fails RBI is not going to save it. Lastly look for LIC stake if the bank has struggled because that is a very good indicator of government support and interest. This is why I would not touch Yes Bank but am ok with IDFC First

LikeLiked by 1 person

Thanks Aditya! Appreciate it!

LikeLike