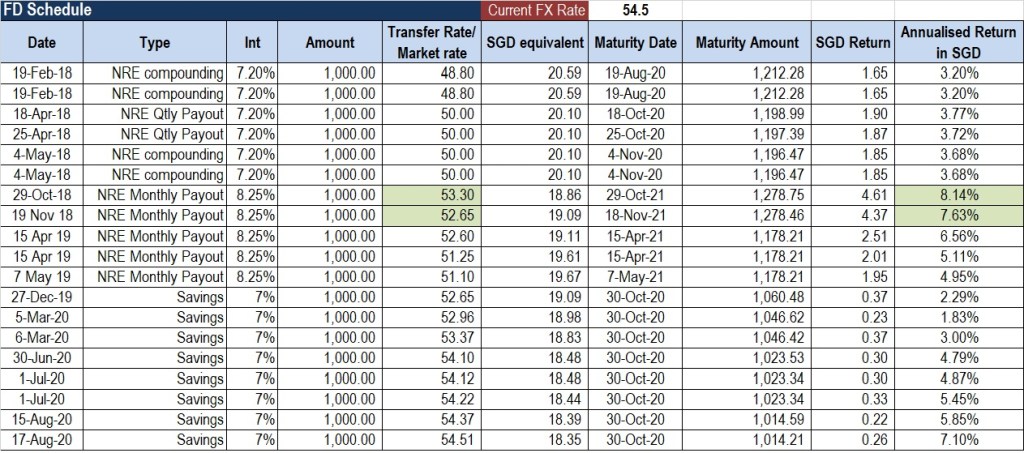

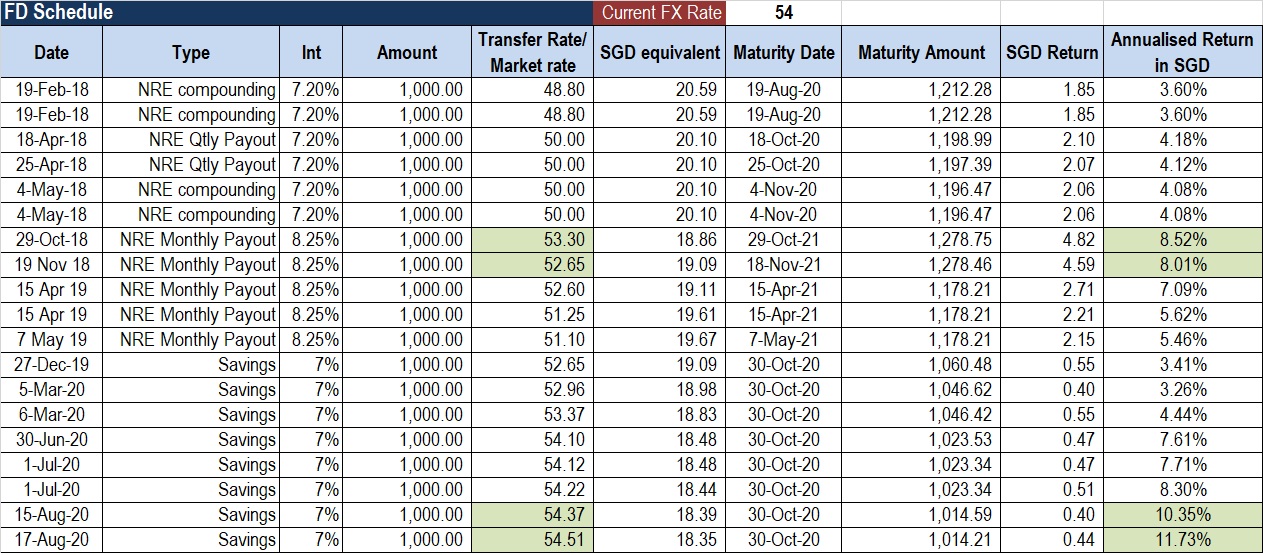

NRE FD has been my preferred low risk, tax free investment option since the time RBI allowed banks to offer interest rates of their choice. However, with the established banks offering only 5% or lesser rates on NRE FD’s, I have been looking for other options that can give higher returns but with same low risk.

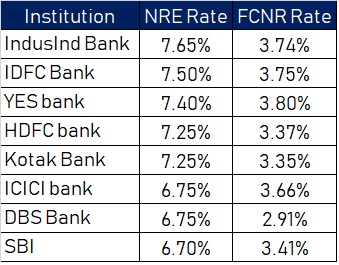

A few banks like IndusInd still offer 6.5% rate on NRE FD but with bank deposits being insured only upto 500,000 rupees the risk of loosing money in case of a default goes up (do remember what happened to Yes Bank and other co-operative banks). A bank will only offer interest rate higher than the market rate under 2 scenarios – either they are a new player and want to build a customer base or they are unable to raise funds easily as markets believe their business to be risky.

Bharat Bond ETF is one such instrument that has been on my radar and I wanted to analyse how it stacks against the NRE FD.

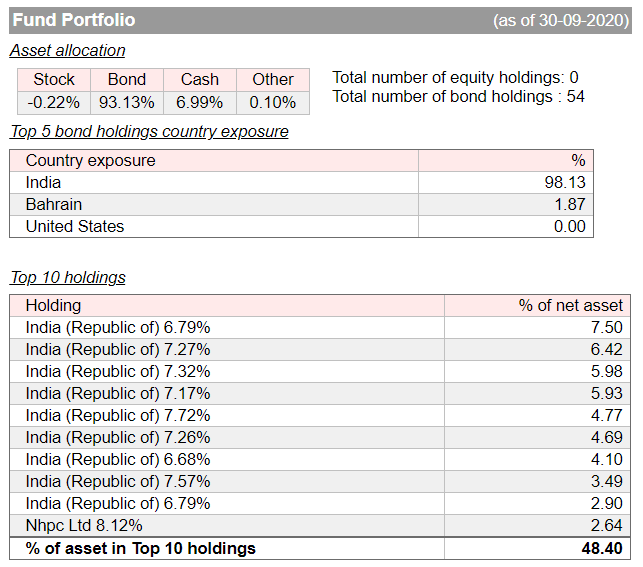

What is Bharat Bond ETF?

Its a Fixed Maturity ETF that invests in AAA rated bonds of Public Sector Companies (PSU). These bonds are not the same a Government Bonds (G-Sec’s) but pretty close in terms of risk profile given that govt has majority stake in most PSU’s.

As this is an ETF, an investor can sell the investment anytime on the National Stock Exchange (NSE), thus being extremely liquid. Yes, there would be short term or long term capital gains depending upon the date of sale but calculations suggest that its a good investment even with taxes if held to maturity.

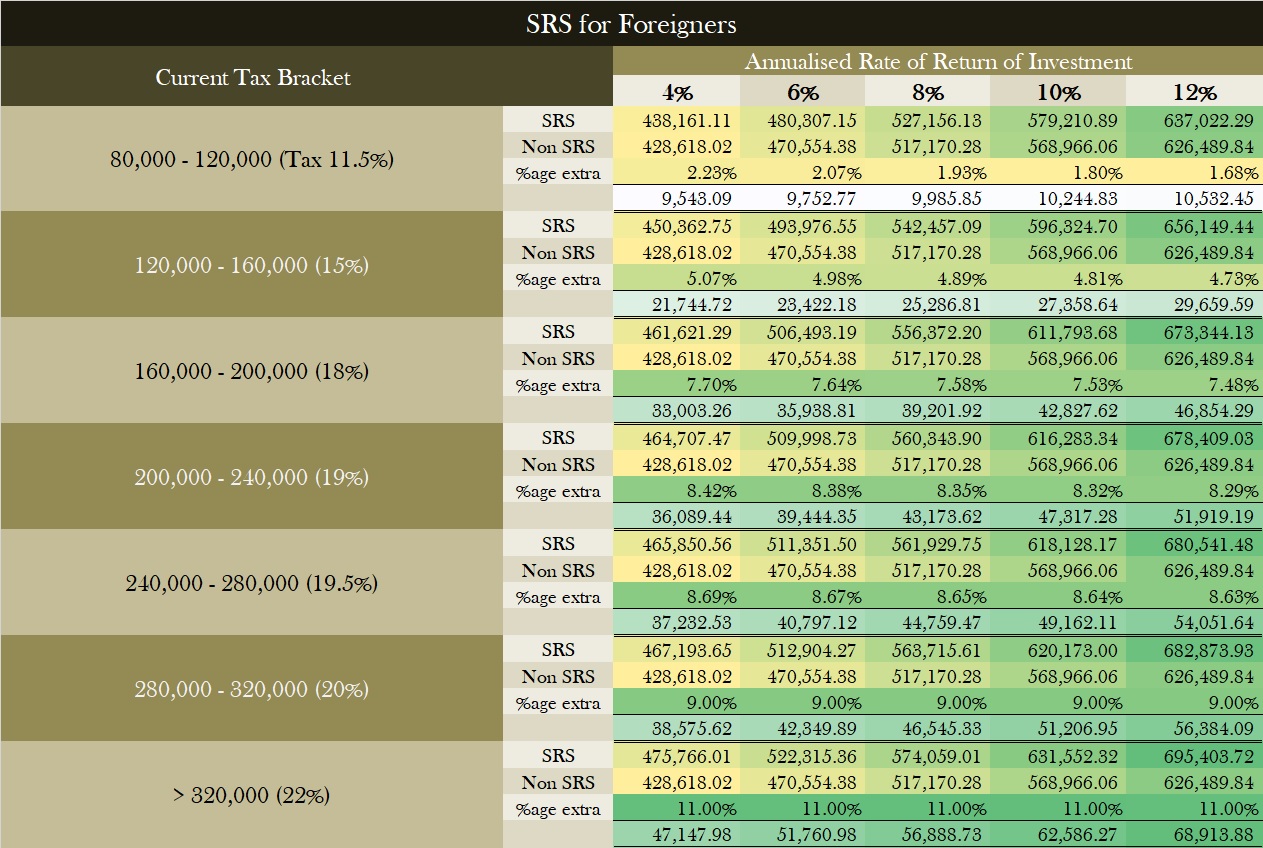

How does it compare to NRE FD?

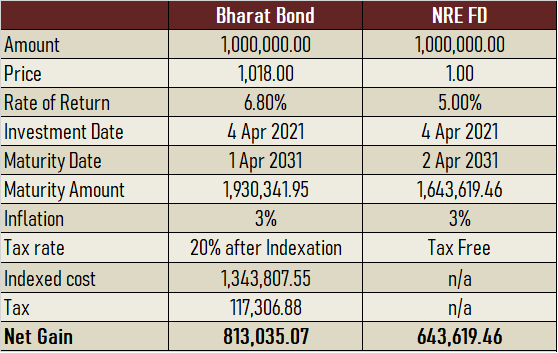

BHARAT Bond ETF wins hands down even after providing for tax when compared to NRE FD’s from large banks.

For calculations, I have assumed that the investor holds the etf to maturity and inflation averages 3%.

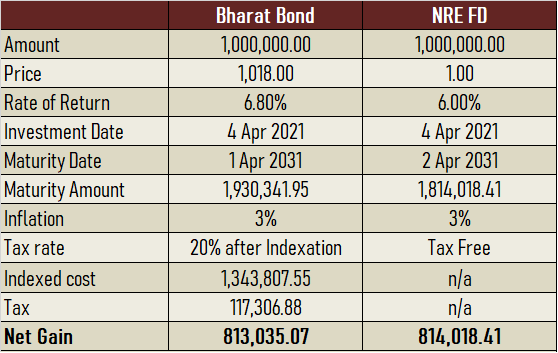

The break even interest differential between the two investments is appx 0.8% with the above assumptions of maturity and inflation. What that means is, in theory, if Bharat Bond ETF yields 6.8% then an NRE FD of 6% will provide roughly the same total return.

Why is Bharat Bond ETF better than NRE FD?

One has to consider multiple factors when considering an investment and not just the yield. The most important factor would be liquidity, default risk and tax impact if you return to India. Bharat Bond ETF provides better risk protection on amounts greater than 500,000 when compared to NRE FD and more liquidity as it is traded on exchange.

Bharat Bond ETF is a better investment than NRE FD irrespective of the interest rate if you have plans to return to India over next 8 years (the tax free benefit of an NRE account ceases within 2 years of returning to India) as the interest from deposits will no longer be tax free. The sooner your plans to return to India the greater the gains from ETF would be when compared to NRE FD.

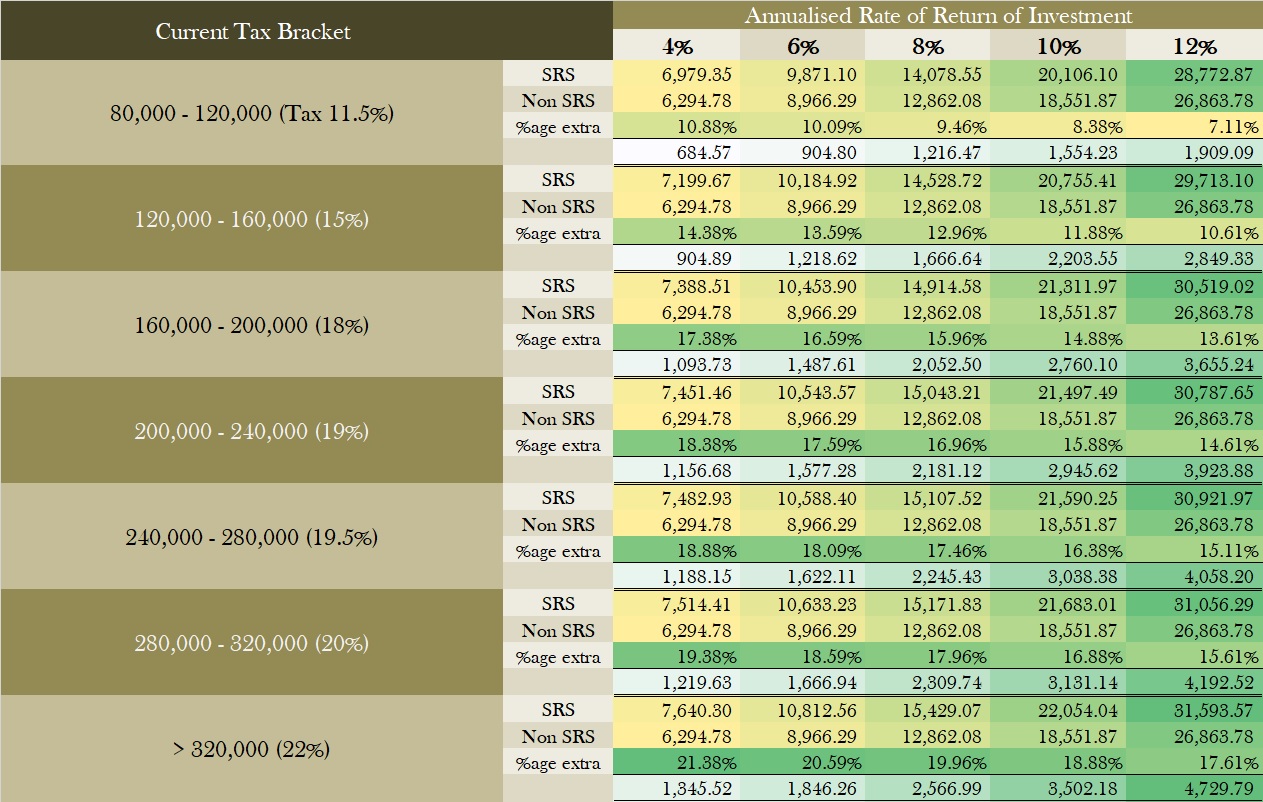

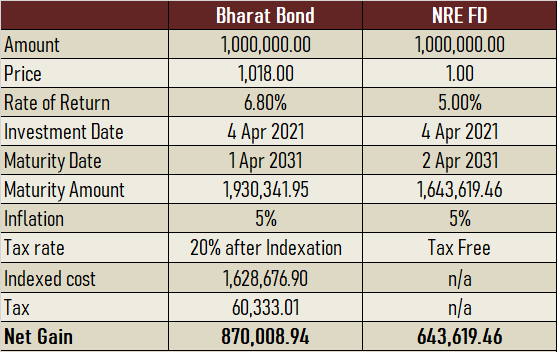

Inflation protection is the other benefit that the ETF provides – If the inflation increases and averages to say 5%, the indexation benefit will reduce the tax liability as shown in table below

Similarly, if the capital gains are removed or the tax rate is reduced in the future the gains from the ETF will be higher.

So no matter how I look at it, Bharat Bond ETF maturing in 2031 is a better investment as compared to NRE FD for long term wealth accumulation. Instead of opening a fixed deposit buying this ETF makes a lot more sense for all investors whether non resident or resident.