Yes, every now and then I do research and analyse avenues that can generate total returns that Trump (no pun intended 😊) the good old NRE FD.

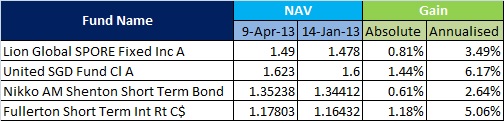

Back in 2016 I had suggested Tax free bonds as a good investment bet (Tax free bonds better than NRE FD’s). The tax free bonds are already up 50% and have also given 7.65% tax free interest year on year which would push up the overall yield to roughly 20% per annum and total return around 85%.

Around a year or more back I talked about India focused SGD denominated debt funds that are available in Singapore in the comments section but never got a chance to do a detailed write up hence now there is detailed analysis.

The fund that I like comes from HSBC – HGIF India Fixed Income AM 30 fund. This has generated better returns than NRE FD over the past year and I believe will continue to out perform over the next year.

HSBC India Fixed Income AM30 fund

Taking the investment date of 22 Nov 2019 when the NAV of the fund was 8.559, the fund has generated 0.42 in dividend till date and fallen slightly to 8.43, bringing the total return to 2.96%.

Comparatively the same amount invested in an NRE FD at 7.5% would have yielded 3.23% if one took the exchange rate of 52.84 (interbank rate). You and I would have got a exchange rate of 52.55 and that would result in a total return of 2.66%. If I factor in the cost of transferring funds back to Singapore the returns will be even lower – 2.1%.

If you did a monthly SIP with this fund the 1 year currency movement adjusted return would have been upwards of 6%.

Downside Risks

With an average yield and good portfolio mix mostly in Govt Sec the downside will only happen if

1. Rupee weakens due to covid or border tensions

2. RBI increases deposit rates due to Inflation

Exchange rate movements impact the fixed deposit returns as well which I had detailed in – Why timing is so important, so from that perspective there is no real difference between this fund and an NRE FD.

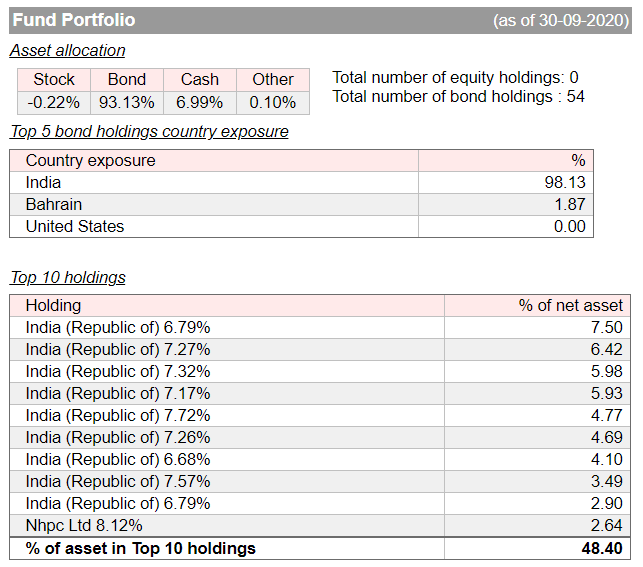

Comparing on account of safety there is not much difference either, NRE FD is insured for a max of 500,000 rupees ~ 9000 SGD and this fund invests in mostly in Indian government or PSU bonds (data below from the fund website) therefore I would think that this fund is relatively safer for larger amounts of investments

Why do I like this fund for money that I want to keep in Singapore?

The fund has additional gains when INR appreciates and investment income in Singapore are tax free. Biggest benefit is liquidity – there is no lock in period like a Fixed deposit and i can sell the units anytime if I need the money. This fund is SRS eligible as well.

It will be worth analysing how this fund stacks against the Bharat Bond ETF, something for a subsequent post. In case you have come across investments that generate relatively safe and superior returns then do mention in comments for everyone’s benefit.