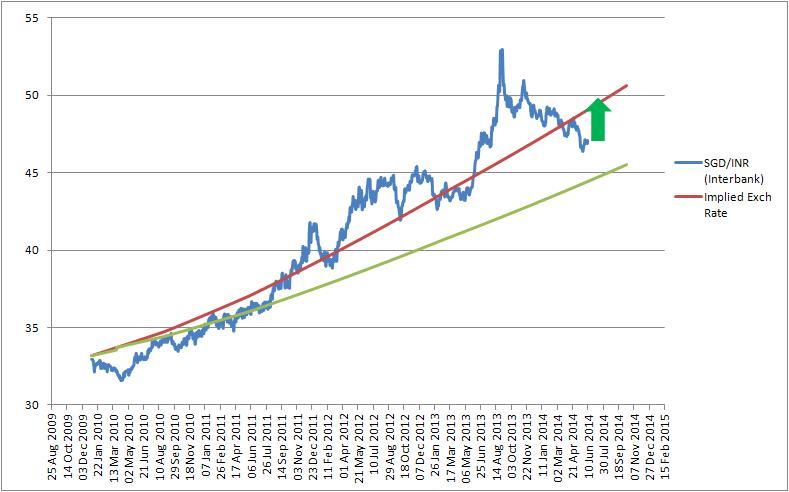

Now don’t tell me you haven’t wondered if SGD can fetch 50 Rupees per dollar 🙂 and I have to admit that with the current rupee weakness it does not look like a impossible number to achieve.

What’s transpired in past 2 months is nothing short of shocking…personally I never thought that the INR could go past the 60 mark against the US Dollar but then I did not expect the Indian Government to bring in the food security bill, in its current format either, which would cost 3.8% of GDP.

The GDP has already been shrinking and GDP growth is estimated to be well below the 6.5% mark as targeted earlier. With rampant red tape blocking foreign investment, tax evasion and upcoming elections the picture doesn’t look to change dramatically in the near future.

On 8th July the rupee breached the 61 mark against the USD and forced the RBI to step in with measures to stem the fall. Since then rupee has stayed below the 60 mark with a weak undertone.

On the other hand the Singapore economy posted a 3.7% growth for the second quarter of 2013. It was more than 15% growth on a quarter by quarter basis. The results looked good but the guidance does not suggest that the trend would continue.

In the meantime, to moderate the housing market, the Singapore government has come up with total Debt Servicing framework which promotes prudent borrowing practices. The SGD in the same time touched 1.28 and has sea-sawed between 1.25-1.28 mark.

So here is what I think is going to happen – The Singapore dollar would weaken towards the 1.30 mark against the USD. This would do well for the Singapore’s exports and the tourism industry. With the weakening of SGD there are rumours that the borrowing rates would slowly increase to keep the housing markets in check. I personally feel that the debt servicing framework is the first step to ensure residents don’t over leverage while buying a property and get in trouble when the interest rates move up.

So as always million dollar question remains what happens to the SGD INR 🙂

My take is that with INR at 60 and RBI showing resolve to not let is fall below and SGD hovering around the 1.26-1.27 mark the mean price for SGD would remain at 47. If the SGD weakens to 1.30 as expected and Rupee settles at 58 SGD INR should march back below the 45 mark.

However if the RBI measures fail to have an impact the Rupee could weaken to 63 against the USD, mainly on account of rising oil prices which are the biggest drain on India’s foreign reserve. If that scenarios plays out then their is little to stop the SGD INR to touch the 50 mark.

However if I look at the Big MC Index the Rupee is undervalued by almost 60% using the purchasing power parity – more on that another day