After a long hiatus I finally got some time to make a post, thanks to the followers for the prompt and encouragement.

SGD INR has been on a roll in the past 8 months and to be honest this move was long overdue. The Indian Rupee was grossly overvalued and just needed a trigger to correct. This time around the triage of rising oil prices, increasing fed rates & falling emerging market currencies led by Turkey and political environment turning less favourable for the ruling BJP led by Prime Minister Modi finally precipitated the Rupee.

Rupee was 47.5 against the SGD and 63.65 against the USD on 1st Jan this year. Since the start of the year the Rupee has fallen 11.5% against the USD and 9% against the Singapore dollar and traded at 71 against the USD and 51.75 against the SGD yesterday. Looking at Year to Date (YTD) values one might think that the move is extreme and Indian economy must have worsened dramatically during the year but the fact is that the currencies were slowly adjusting to the dollars rise over the past 2 years and rupee was irrationally holding its ground. I have often mentioned in my previous posts that strength of currency and national pride should not be linked and currency should follow economic fundamentals and why such a simple concept evaded the current Indian government is beyond my comprehension.

Delving a little deeper and looking at the currency movement from an academic angle and using the Interest rate parity, the Fed rates have moved up from 25 basis points to 200 basis points over the past 2 years. India increased its rates recently from 6% to 6.25%. The interest rate differential which used to be around 6% has now come down to 4%. One might say that should have resulted the rupee falling by only 2% (6% – 4%) but why the big fall?

The answer is that rupee was fundamentally over valued. At the start of the year the REER (Real Effective Exchange Rate) index stood at 118 which simply means that the currency was 18% overvalued against a basket of currencies. The index currently is around the 110 mark. Which indicates that even after the correction the rupee remains overvalued. Now does that mean that rupee could fall another 10% against the US dollar? The answer is, theoretically yes! but will it happen in real, I don’t think so.

How does the rest of the year look like against USD?

The Fed is on a war path to increase interest rates and I expect at-least 2 more hikes over next 9 months before they take a breather. Oil prices have stuck around the US$75 mark and the expectation is for the oil demand to boost prices to US$80 to 85 a barrel range. The shock would have been severe had the world not been investing in alternative sources of energy. The US economy has been doing exceptionally well and the unemployment is at an all time low, EU has also started to improve with lower unemployment. After effects of BREXIT are still a concern and the ongoing trade war between US and the rest of the world doesn’t look to stop any time soon.

I think that the USD INR has a little more room to drop and will stabilise around the 72-74 range, another 2 to 4% decline from current levels. RBI has been smart to not defend the rupee unnecessarily and burn through the reserves learning from the actions of the other central banks and is in the market to just smoothen the rupee’s fall. However, better than expected GDP figures published on 1 Sep should lend temporary support to the rupee.

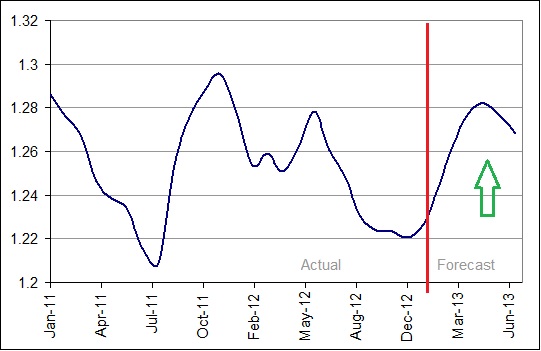

What does it mean for SGD INR?

Singapore dollar has been less impacted by the strengthening USD and MAS has allowed the currency to strengthen to neutralise the increasing US interest rates. USD SGD has hovered around the 1.35-1.37 mark.

If the fundamentals in the market deteriorate dramatically, USD SGD could touch 1.40, however if the oil prices increase and the inflation, specially housing prices don’t cool down the currency could strengthen to 1.30.

The SGD INR range that I see for the rest of the year would be between 50 to 54, with a bias to stabilise around the 52.5 mark.

India has elections due next year and this currency weakness would be welcome by the ruling party, which has a large support amongst the overseas Indian community to have foreign donations resulting in bigger rupee conversions. This is not very different to what happened in 2014 when the rupee had depreciated to 53 against the SGD in Aug of 2013 and then slowly recovered as elections approached in 2014. I am pretty confident that the trend will be repeated this time around.

Finally, coming to the crucial question of will rupee touch 55? I don’t think so.

Should you convert now and remit to India or wait? this is dependant on individual circumstances though I personally like to keep funds invested in Singapore.