Its been a few months since I wrote about the pair as most of the discussions were in comments to previous posts, but today’s MAS decision warranted a new post.

There were ripe speculations that MAS is going to ease the monetary policy (which it did) and Singapore is headed for a technical recession. The economy expanded by a modest 0.1% much against the consensus of a contraction of 0.1%. The immediate impact on the exchange rate was a modest gain from 1.4025 overnight to 1.3960 as I write.

One would question that why has SGD strengthened even though the policy has been slightly eased? There are various factors at play:

- The expectations of a USD rate increase this year are negligible. I would be surprised if the Fed raised the rates in Dec when the volumes are thin due to holiday season. My personal view is that it was a missed opportunity in Sep and Fed should have increased the rates but that’s a different topic of discussion.

- SGD had fallen all the way to 1.43 in anticipation of easing, but recovered slowly over the past week with rest of the regional currencies. If one looks at the bigger picture then Indonesian Rupiah has appreciated by around 9% against the USD and Malaysian Ringgit has firmed up by around 6% in past 10 days. The key words for me from the MAS policy statement is “slow the pace of local dollar’s gain”

MAS will continue with the policy of a modest and gradual appreciation of the Singapore Dollar Nominal Effective Exchange Rate (S$NEER) policy band. However, the rate of appreciation will be reduced slightly. There will be no change to the width of the policy band and the level at which it is centered, saying it would seek to slow the pace of the local dollar’s gains versus its trading partners.

Both Malaysia and Indonesia are key trading partners for Singapore and a greater than 5% jump in their currencies diluted any chance of SGD depreciation. The intent of MAS Is clear – it wants SGD to be slightly stronger than its trading partners.

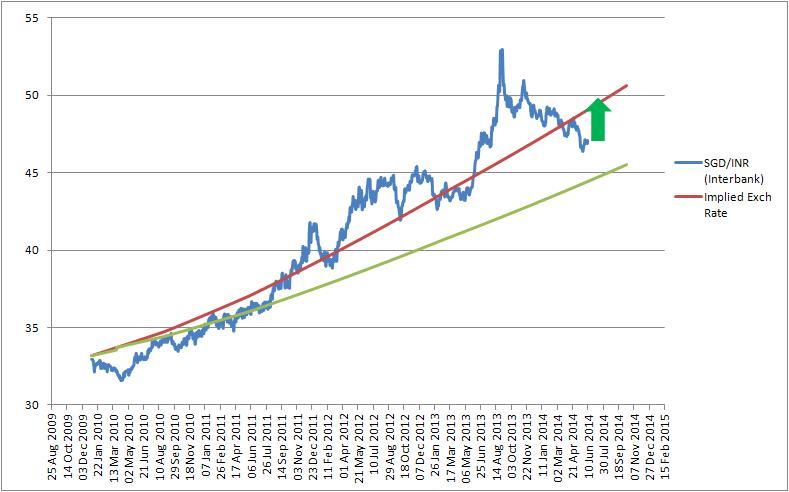

Now if one looks at INR it appreciated very quickly in after the US job reports from the comfort that no fed hike is on the cards. It was good news for FII’s who can pump money in Indian Bonds and earn good interest rate. Many mistake this as FII investment in India because if one looks at the economic indicators they don’t look very good – be it industrial production. agriculture produce or job growth.

I have said this many times and would repeat again – the sooner INR falls towards 70 the better it is for India. The Indian exports are declining due to competition from other countries with weaker currencies and the day fed hikes the interest rate INR could dip 2-3% overnight and that is not a pleasant shock for the economy.

Anyway for now no major events are scheduled in the coming months other that the results of the BIHAR elections. I believe irrespective of the outcome the Rupee is scheduled to fall post-election results. If BJP wins there would be a knee jerk appreciation which will fizzle out as the economic data and realities will take center stage. If BJP looses then Rupee would immediately fall from a sentiment perspective.

So for the next few weeks I expect SGD INR to be range bound between 46-48.