With RBI reducing benchmark rates the NRE FD rates have been on a decline though some banks still offer high returns.

NRE Interest is tax free but only guaranteed protected upto a maximum of 5 lac rupees just like any other bank deposits, anything over that is like a unsecured loan to the bank.

So while making a deposit try and spread the risk across different banks if possible. Yes, that means having to manage more than one bank account and if you like the convenience go for a respected and strong bank like SBI though it means lesser return.

When shortlisting a bank, I would not touch a co-operative bank no matter how high a rate they offer, then I would exclude small time private players, then exclude big private players who have grown too fast (remember Yes Bank), then look at Balance sheet and management and even exclude foreign banks like Deutsche and HSBC whose parent entities are struggling. If any foreign bank fails RBI is not going to save it. Lastly look if LIC has a stake in the bank, if yes, then that is a very good indicator of government support and interest (higher chance of bailout if something goes awry).

Click on the Bank Name in the table above and it will take you to the website of the Bank and if you find any other rates that are worth sharing leave a comment and I will add them to the table.

Yes, every now and then I do research and analyse avenues that can generate total returns that Trump (no pun intended 😊) the good old NRE FD.

Back in 2016 I had suggested Tax free bonds as a good investment bet (Tax free bonds better than NRE FD’s). The tax free bonds are already up 50% and have also given 7.65% tax free interest year on year which would push up the overall yield to roughly 20% per annum and total return around 85%.

Around a year or more back I talked about India focused SGD denominated debt funds that are available in Singapore in the comments section but never got a chance to do a detailed write up hence now there is detailed analysis.

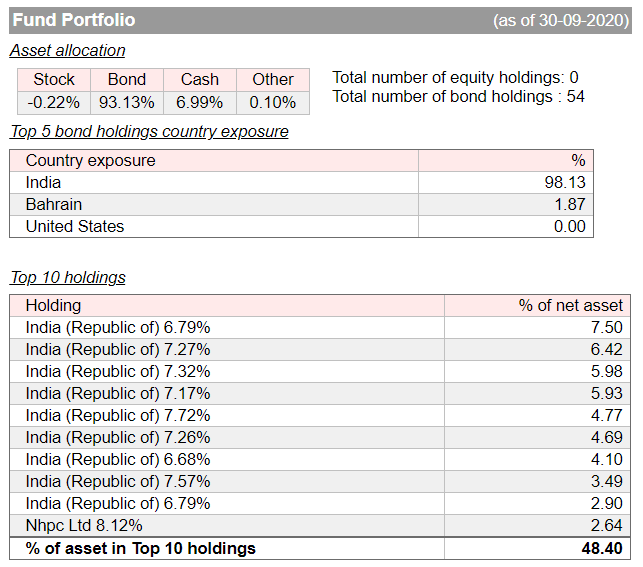

The fund that I like comes from HSBC – HGIF India Fixed Income AM 30 fund. This has generated better returns than NRE FD over the past year and I believe will continue to out perform over the next year.

HSBC India Fixed Income AM30 fund

Taking the investment date of 22 Nov 2019 when the NAV of the fund was 8.559, the fund has generated 0.42 in dividend till date and fallen slightly to 8.43, bringing the total return to 2.96%.

Comparatively the same amount invested in an NRE FD at 7.5% would have yielded 3.23% if one took the exchange rate of 52.84 (interbank rate). You and I would have got a exchange rate of 52.55 and that would result in a total return of 2.66%. If I factor in the cost of transferring funds back to Singapore the returns will be even lower – 2.1%.

If you did a monthly SIP with this fund the 1 year currency movement adjusted return would have been upwards of 6%.

Downside Risks

With an average yield and good portfolio mix mostly in Govt Sec the downside will only happen if

1. Rupee weakens due to covid or border tensions

2. RBI increases deposit rates due to Inflation

Exchange rate movements impact the fixed deposit returns as well which I had detailed in – Why timing is so important, so from that perspective there is no real difference between this fund and an NRE FD.

Comparing on account of safety there is not much difference either, NRE FD is insured for a max of 500,000 rupees ~ 9000 SGD and this fund invests in mostly in Indian government or PSU bonds (data below from the fund website) therefore I would think that this fund is relatively safer for larger amounts of investments

Why do I like this fund for money that I want to keep in Singapore?

The fund has additional gains when INR appreciates and investment income in Singapore are tax free. Biggest benefit is liquidity – there is no lock in period like a Fixed deposit and i can sell the units anytime if I need the money. This fund is SRS eligible as well.

It will be worth analysing how this fund stacks against the Bharat Bond ETF, something for a subsequent post. In case you have come across investments that generate relatively safe and superior returns then do mention in comments for everyone’s benefit.

SGD INR finally crossed 55 after appreciating 5% from the exchange rate in Nov 2019 – 52.60. Theoretically speaking you would have gained slightly more by transferring to India but after accounting for the transaction costs it might not have been much.

It stayed below the 55 mark as I had written more than 2 years back SGD INR flirts with 52 could it hit 55. That time i did not think it will cross 55 but now I am updating my SGD INR target to 57, yes you read it right, Fifty Seven!!

By when?

I expect this to be achieved by the end of the year and then the rate should slowly decline back to 54.5 leading upto the Indian Budget in Feb 2021

The rationale being that USD INR will touch 76.5 and USD SGD will move to 1.34 mark in the short run.

Why will INR weaken?

Inflation and rising COVID cases will make it hard for INR to appreciate, the fund flows on account of mega deals that Reliance Industries has been doing should come to an end and at some point the Foreign Institutional investors will book profits and withdraw their gains from the stock markets. RBI will smoothen then currency movements but given the inflation has very little room to tweak the interest rates.

Why would SGD strengthen?

Singapore is one of the last few countries that offer a positive interest rates on government securities and is politically stable unlike US or parts of Europe. This gives SGD bonds safe haven status and money comes in. The same thing happened in 2009-2012 when SGD rose to as high as 1.22 against the USD.

Does this only benefit SGD INR?

Next 6 weeks should provide opportunity across currencies – EUR INR could see 90, GBP INR 99 and USD INR – 76.5. So those looking to transfer can watch out for these levels.

Instead of waiting for absolute levels, I would plan for any transfers based on what is your end goal. If you are getting a high interest rate in NRE FD’s or other investments now then even current rate of 55.4 is a good rate. Each of us have different goals, tax status and risk tolerances. Therefore plan based on your needs and not get stuck at specific levels.

There are other options if you do not want to transfer the money to India and yet want to gain with the short term increase in rates, watch out for the next post.

While it maybe difficult to time any market timing does play an important role and could be the difference between ordinary and stellar returns.

Timing of transferring money to India and investing in NRE Deposits or any other investment vehicle could also mean the difference between a 3% compounded return vs returns of 7% or more.

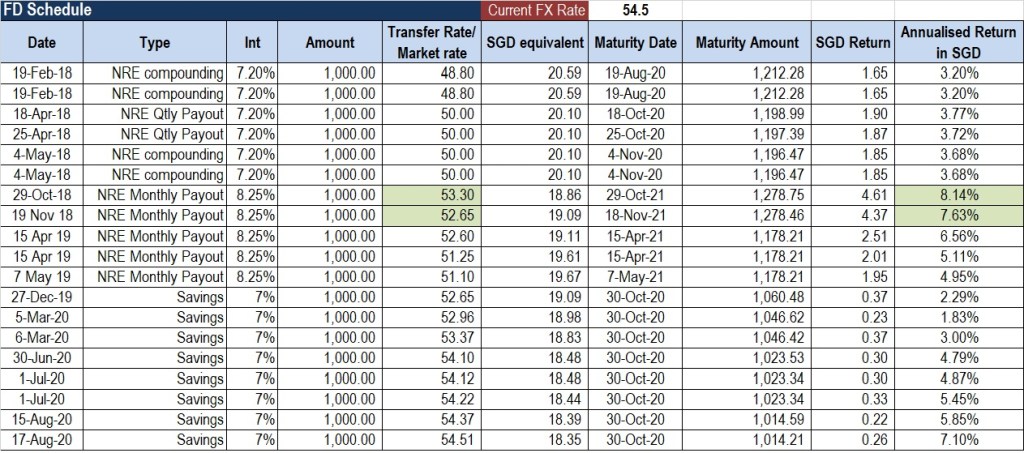

To illustrate this, I took the money transfers I have done over the past few years and tabulated a return table. I factored in cost of transferring funds i.e. nett money received in India and also the cost of repatriating the money back on maturity and using today’s exchange rate

As you would see the return ranges from anywhere between 3% to 8%, even for transfers which were done not too far apart.

The best returns were achieved when the SGD INR rate was well beyond what fundamentals commanded – like in 2018 the fair value of SGD INR was around 52 and a transfer made at 53.3 generated a superior return

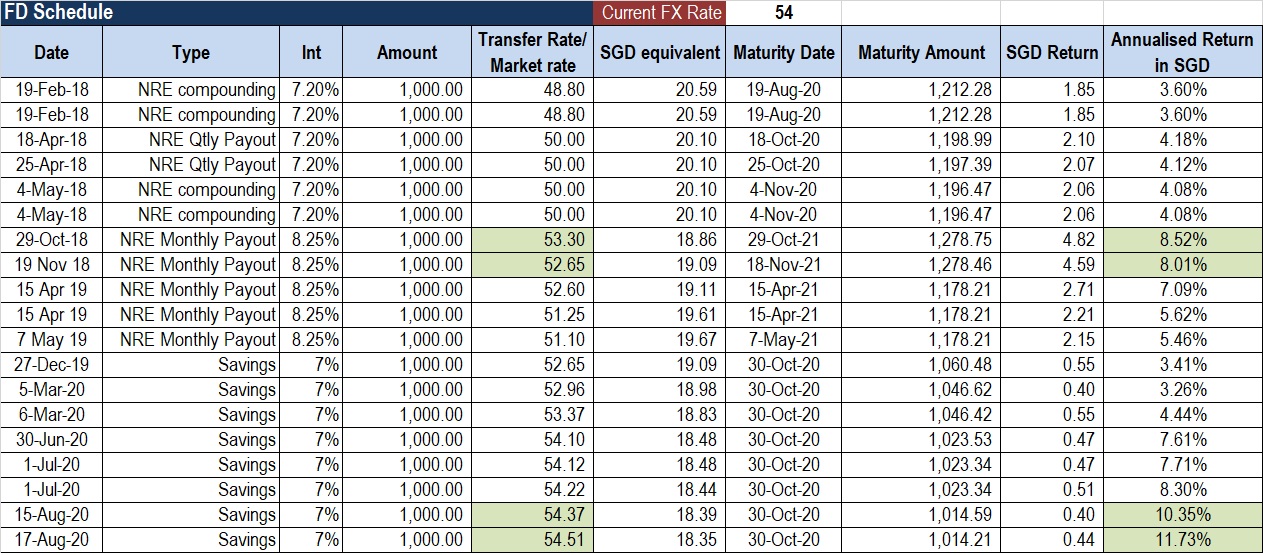

If the exchange rate moved favorably or stayed flat the returns went up. Return matrix using exchange rate of 54

Based on long term interest rate parity, i believe 54.5 -55 is fair value for SGD INR towards the end of 2020. So if the pair crosses 55 and banks are still offering 6% or more NRE FD’s then it would be a good investment to consider.

I would be keen to hear what your experience with generating stable returns in India has been

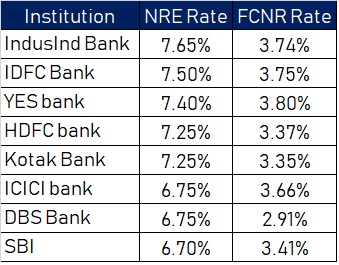

Travelling from Busan to Seoul on a train gives ample time to think about the question many of you have asked – Is it worthwhile to invest in FCNR deposits?

Instead of looking at purely FCNR deposits I decided to do a comparison between FCNR deposits and the good old NRE deposit.

The analysis did become a little tricky as the SGD FCNR deposits have ridiculously low-interest rates and there is no SGD INR forward cover that is readily available in the market and I had to use USD for comparisons.

First of all, lets look at the NRE and FCNR deposit rates on offer in the market for a one year period.

NRE and FCNR Interest rates as on 11 Sep 2018

Using the best available rates for both NRE Fixed deposit and FCNR deposits we have the below payoff for a one year maturity and expected USD INR rates.

Depositing money in USD deposits in Singapore

This is probably the worst of all the options. The best possible rate for USD deposits in Singapore is 2% and banks charge anywhere between 0.5% to 0.7% to convert SGD to USD and back from USD to SGD. Though one would often see the advert say that there are no charges but the cost is built-in the exchange rate. With the cost of converting money the yield turns out to be mere 0.5%. So unless you are expecting a massive Singapore dollar weakness against the USD this option is best avoided. It is better to keep your money in BOC Smart saver account for better yields.

Investing in USD FCNR with a one year forward cover

The costs involved here are 0.7% to convert SGD to USD, cable charges of atleast 30S$ to transfer money to FCNR account, cost of a forward cover in terms of margin money and brokerage and finally the cost of converting USD back to INR or to SGD and remitting back to Singapore.

With all the associated costs, this option would work if you expect the INR to strengthen back and want to lock the exchange rate at current forward rate of 75. Here the interest on FCNR deposit is tax free but the gains or losses on the forward cover will attract taxes and on the pay off matrix it is not a great option.

Investing in NRE FD

The cost here is simply one time money of 0.5% to transfer money to NRE account and cost to transfer money back if one so desires.

This option gives the stable returns without any complicated transaction setup.

Investing in USD FCNR deposit without a forward cover

The costs here, as in option 2 above, are 0.7% to convert SGD to USD, cable charges of $30 to transfer money to FCNR account and the cost of converting USD back to INR or to SGD and remitting back to Singapore.

Depending upon one’s outlook for USD INR this option can give good returns. If Usd INR crosses 76 over the next year then this option gives better returns than NRE FD but if INR strengthens then one might lose any gains made from interest income.

FCNR NRE Pay Off

So what is the recommendation?

Given the increased uncertainty in global markets predicting the USD INR rate 1 year rate is nothing short of speculation. I personally do not think the USD INR will cross 77 or even if it crosses will stay at that level at the end of one year. To do the FCNR deposit for a very, very small gain over NRE deposit in the event USD INR crosses 76 does not look great from the risk reward perspective but if you really want to try then put half your money in NRE FD and the other half in USD FCNR deposits.

After a long hiatus I finally got some time to make a post, thanks to the followers for the prompt and encouragement.

SGD INR has been on a roll in the past 8 months and to be honest this move was long overdue. The Indian Rupee was grossly overvalued and just needed a trigger to correct. This time around the triage of rising oil prices, increasing fed rates & falling emerging market currencies led by Turkey and political environment turning less favourable for the ruling BJP led by Prime Minister Modi finally precipitated the Rupee.

Rupee was 47.5 against the SGD and 63.65 against the USD on 1st Jan this year. Since the start of the year the Rupee has fallen 11.5% against the USD and 9% against the Singapore dollar and traded at 71 against the USD and 51.75 against the SGD yesterday. Looking at Year to Date (YTD) values one might think that the move is extreme and Indian economy must have worsened dramatically during the year but the fact is that the currencies were slowly adjusting to the dollars rise over the past 2 years and rupee was irrationally holding its ground. I have often mentioned in my previous posts that strength of currency and national pride should not be linked and currency should follow economic fundamentals and why such a simple concept evaded the current Indian government is beyond my comprehension.

Delving a little deeper and looking at the currency movement from an academic angle and using the Interest rate parity, the Fed rates have moved up from 25 basis points to 200 basis points over the past 2 years. India increased its rates recently from 6% to 6.25%. The interest rate differential which used to be around 6% has now come down to 4%. One might say that should have resulted the rupee falling by only 2% (6% – 4%) but why the big fall?

The answer is that rupee was fundamentally over valued. At the start of the year the REER (Real Effective Exchange Rate) index stood at 118 which simply means that the currency was 18% overvalued against a basket of currencies. The index currently is around the 110 mark. Which indicates that even after the correction the rupee remains overvalued. Now does that mean that rupee could fall another 10% against the US dollar? The answer is, theoretically yes! but will it happen in real, I don’t think so.

How does the rest of the year look like against USD?

The Fed is on a war path to increase interest rates and I expect at-least 2 more hikes over next 9 months before they take a breather. Oil prices have stuck around the US$75 mark and the expectation is for the oil demand to boost prices to US$80 to 85 a barrel range. The shock would have been severe had the world not been investing in alternative sources of energy. The US economy has been doing exceptionally well and the unemployment is at an all time low, EU has also started to improve with lower unemployment. After effects of BREXIT are still a concern and the ongoing trade war between US and the rest of the world doesn’t look to stop any time soon.

I think that the USD INR has a little more room to drop and will stabilise around the 72-74 range, another 2 to 4% decline from current levels. RBI has been smart to not defend the rupee unnecessarily and burn through the reserves learning from the actions of the other central banks and is in the market to just smoothen the rupee’s fall. However, better than expected GDP figures published on 1 Sep should lend temporary support to the rupee.

What does it mean for SGD INR?

Singapore dollar has been less impacted by the strengthening USD and MAS has allowed the currency to strengthen to neutralise the increasing US interest rates. USD SGD has hovered around the 1.35-1.37 mark.

If the fundamentals in the market deteriorate dramatically, USD SGD could touch 1.40, however if the oil prices increase and the inflation, specially housing prices don’t cool down the currency could strengthen to 1.30.

The SGD INR range that I see for the rest of the year would be between 50 to 54, with a bias to stabilise around the 52.5 mark.

India has elections due next year and this currency weakness would be welcome by the ruling party, which has a large support amongst the overseas Indian community to have foreign donations resulting in bigger rupee conversions. This is not very different to what happened in 2014 when the rupee had depreciated to 53 against the SGD in Aug of 2013 and then slowly recovered as elections approached in 2014. I am pretty confident that the trend will be repeated this time around.

Finally, coming to the crucial question of will rupee touch 55? I don’t think so.

Should you convert now and remit to India or wait? this is dependant on individual circumstances though I personally like to keep funds invested in Singapore.

It’s been really long since I wrote a post dedicated to SGD INR and as 2018 fast approaches time is ripe to share my views on how SGD INR could move in the following months.

Given the politically volatile times that we live in and dilemma the central banks in developed economies face with prolonged period of low inflation, a few interesting scenarios might play out.

Starting with India, with the implementation of demonetization and GST the countries GDP has taken a hit, which was not entirely unexpected. Any country that has implemented GST, experienced turbulent time of approximately 18 months before the benefits started to roll in. Alongside the GST implementation, the government has also been aggressively pushing for interest rate cuts to increase the economic activity. However, with the recent inflation print which came above expectations and crude oil prices persisting above 50 USD a barrel, the chance of rate cut in December ’17 is next to zero. The risk of inflation further accelerating is high and RBI has rightly held off reducing rates further until there are signs of moderating / low inflation. Now, a lot of this can be resolved if the manufacturers/producers start passing the benefits of reduced taxes from implementation of gst to consumers, this would result in reduced prices, which will lead to lower inflation and set the stage for a RBI rate cut but structural reforms of this scale take time to fine tune.

On the political front, the elections in prime ministers home State of Gujarat are scheduled in less than a months time followed by a few more states with the National elections soon in sight in 2019. Any upset in the elections or signs of losses to the ruling party will result in re-evaluation of investor sentiment in India.

Now looking at the global factors, the 2 major central banks have diverged their monetary policies with Federal Reserve firmly on a path of rate hikes and ECB continuing with its Bond Purchases and negative interest policy well into September 2018. Japan has also indicated to continue with ultra loose monetary policy until inflation hits 2%. How did central banks arrive at this 2% magic figure is still beyond my understanding but that is a topic for another post.

With the US Federal Reserve increasing rates, reducing interest rates will be extremely challenging for RBI and without lowering rates encouraging new investments in India that leads to Job creation a distant dream. A divergence of relative yields between US treasuries and Indian bonds can result in a sudden flight of capital from the country.

At the same time the valuations in the Indian stock markets are at all time highs and the market trades at PE of over 23 which again by historical standards is high and suggests a correction. Infact the global stock markets are trading at an all time high with this liquidity driven rally. With Federal Reserve increasing rates, the investors will be forced to consider cost of capital which could result in market correction and money being taken out of India.

The silver lining amongst all this is that Indias foreign reserves have crossed 400 Billion dollars and that would provide some cushion against external shocks.

In Singapore, the inflation and GDP growth has picked up but is still erratic. Singapore Dollar being a managed currency against a basket of currencies, of which USD, Euro and Japanese are a part of, the policy divergence between US and Europe will be interesting to watch. MAS administers the monetary policy through exchange rate and is maintaining a neutral slope of exchange rate band but with US Treasuries strengthening yield curve how long would this band remain flat is a question worth asking.

Another very important factor not much talked about is the political succession in Singapore. Prime Minister Lee Hsien Loong has expressed his desire to step down as the prime minister or atleast have a succession plan in place. Who will succeed him and the political fall out from that move can impact Singapore economy and SGD.

Singapore is fast trying to re-invent itself and write the next chapter of the growth story by catching on to the fintech wave and bio medical Research. Can these initiatives bring in new investments and create jobs will have to be seen.

So both currencies have their set of political risks and also will be impacted by increasing US interest rates.

Singapore being a smaller economy and having shown greater nimbleness to react to global events is slightly better placed when compared to India making SGD slightly stronger than Rupee on a relative basis.

I believe that just like 2017, 47.50 will play a pivot for the currency pair and we could see a range of 46 to 50 in the coming months as the inflation conundrum plays out – India wanting a lower inflation so that they can cut interest rates and developed world wanting higher so the rate increase cycle can continue.

Finally the tool to compare investment options is here.

Its configured for Indian Tax Rates for FY 2017 -2018 and works pretty accurately – I tried to test as much as I could but feel free to point issues if you find some.

To use the tool simply input your Investment amount and the Total income before this investment. That will calculate your tax bracket.

Then choose the category of investment and input your expected rate of return and the tool will give you the comparative pre and post tax earnings.

The money changers in Arcade, Raffles place are again offering a rate better than the spot rate. The current spot is 47.20 and you could get 47.75 with the money changers.

Again the notes are all legit and there is nothing wrong that I could find.

I could not help but wonder if 2000 Rupee notes will soon be withdrawn and prove the rumours correct. If that happens where will Indian GDP go is anybody’s guess but till then if you are visiting to India then exchanging money in Singapore and carrying back is a profitable bet.

As an NRI, you would have wondered many times, what parts of your Indian Income are taxable and what are not and trust me you are not alone.

Under the Indian Income tax act, the tax rates, deductions from income, exemptions from taxation all change depending on the nature of income and residential status of the individual. With the ever changing tax provisions, even if you searched online the chances of finding the information you are looking for would not be easy and filtering out the tax provisions that are applicable to an NRI is even more difficult.

Not being able to find consolidated tax provisions on common investments used by NRI’s I decided to compile the information myself and hope that fellow NRI’s will find it useful.

NRI’s mostly invest in Fixed Deposits, Bonds, Mutual Funds, Stock and Property which would generally give rise to income under Capital Gains or Other Income (Bank Interest or Dividends) under the Indian Tax laws.

I have tabulated the provisions that an NRI should be aware of for FY 2017-2018 (click on table to open in new window)

One of the most interesting things to note is that the basic tax free exemption is not available to an NRI on Equity Investments. What that means is that if an NRI gained 2,50,000 Rupee by investing in stock market the whole 2,50,000 Rupee is taxable. If these gains are long term (asset held for more than 1 year) then there is no tax liability but for short term gains the tax rate is @ 15%. So an NRI would pay Rs.37,500 in taxes, the income would not attract any tax in hands of a resident Indian.

Another interesting fact to note is that the gains on redemption of Sovereign Gold Bonds are not chargeable to tax if held till maturity.

With difference in tax rules being different in different countries an investor should consider the tax domicile of the investment to maximise returns. In Singapore and Hong Kong the Capital gains, Bank Interest and Dividends are not taxable, however in USA and UK these income are taxable.

For example if an NRI bought a mutual fund in India that returned 20% over a period of 6 months then his gains would be taxed at a flat rate of 15% resulting in a post tax return of 17%. Buying this same fund in Singapore would have been as the gains are tax free and the investor pays no tax.

Similarly for bonds the interest is taxable in India and taxed at the marginal rate based on your income bracket but tax free in Singapore and Hong Kong.

E.g . An NRI whose total income is over Rs. 10 lac (30% tax bracket) buys a bond that pays 9% interest p.a. The post tax yield of this investment would be 6.3% . Add to it the cost of transferring funds to India of around 0.8%, the yield drops to 5.5%. If the plan is to remit the money back to Singapore on maturity, which will cost another 1%, the investment would yield 4.5% only.

These are just 2 examples to get you thinking. There innumerable scenarios that I can come up with based on different countries of residence and each individuals tax profile. All I would like to highlight is that an investor should not underestimate the impact of taxation and ancillary costs while making investment decisions and look at all aspects before making an investment decision.

Watch out for an investment comparison tool that I am working and will post it here very soon. Till then keep reading and sharing.