The much talked about interest rate cut finally happened today. RBI Governor keeping true to his character surprised the markets with an earlier than expected cut taking India on a path different from Russia and Brazil where central banks have increased the benchmark rates in the past few weeks.

I must say it’s a brilliant move by the Governor to put the ball back into Finance Ministers court and push for structural fiscal reforms in the upcoming budget. The general sentiment has been that the higher rates are keeping India from growing which overshadows the fundamental issues of red tape, poor infrastructure and wastage in public expenditure.

The sustained fall in oil prices (thank Russia for occupying Crimea) has given India the much-needed window to push through reforms without being worried about stroking uncontrolled inflation.

The question is that will this rate cut and structural reforms be enough to achieve the targeted growth? No, absolutely not. The other key factor, which should not be ignored, is the exchange rate of the rupee against other currencies. To recap the last year – Rupee has oscillated between 58 and 63.5 against the US dollar (I use USD as a benchmark because the other rates are nothing but a cross rate). The fall in rupee has been less pronounced as compared to its Asian peers like the Malaysian Ringgit, Indonesian Rupiah, Singapore Dollar, Korean Won etc. On the global front, the Yen, Euro and Pound have also dropped sharply against the USD resulting in net gains by the Rupee against these currencies as well.

While the gains in Rupee boost the feel good factor about the India story – is a sustained gain in Rupee the right thing for the Indian economy? My take is that RBI would not let Rupee gain beyond the 62 mark to keep the exports competitive. There was evidence of this when RBI was seen buying dollars in the last week when Rupee gained sharply. With a generally weaker Rupiah, Ringgit, Peso and Riel the Indian exports would face tough competition in areas like garments, IT services, food grains and other manufacturing. Also with Euro and Pound weakening the demand from European countries would decline if the goods are not priced competitively.

With crude oil staying below 50, I think RBI would target the Rupee around 65 against the USD (at-least that’s would I would do, if I were the RBI governor). That would be a roughly 5% decline from the current levels and will bring it at par with other countries with export competitiveness. A sharp gain in the currency would negate any benefit that the lower oil prices would have and I don’t think the RBI or the finance minister would want that.

We should not forget that infrastructure reforms do not happen overnight and take years to fully have the desired impact.

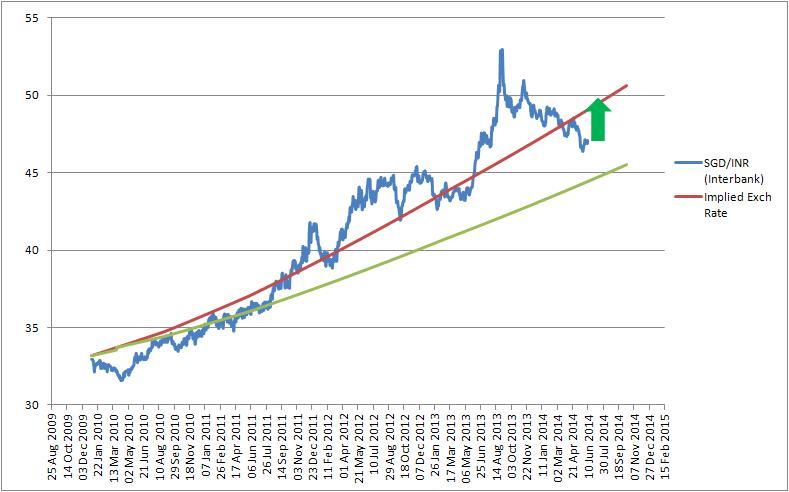

What would that do to SGD INR – 45 mark would remain as the strong support for the pair with upside of Rs.50, but of-course remitting money to India and investing in NRE deposits would always remain a good option.