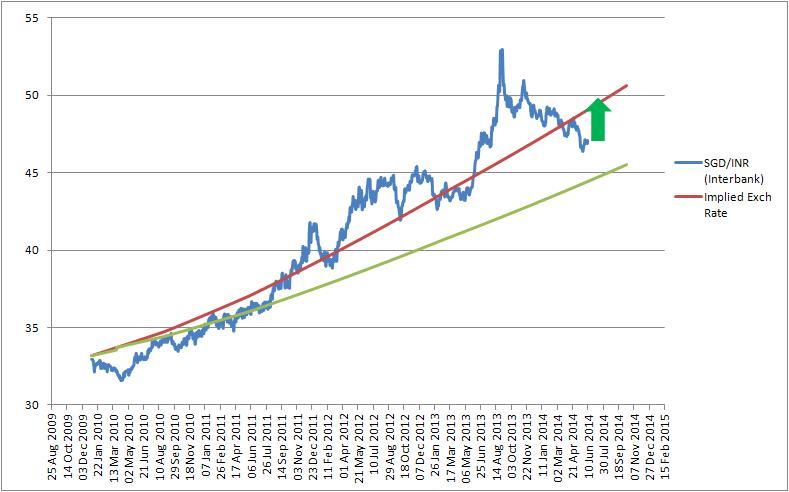

With the jump in SGD INR the question of what is the best way to transfer money to India becomes important and has been asked a few times. My conclusion before today’s analysis was that DBS remit gives the best rates with the smoothest transaction experience. However in such a competitive market innovations and better pricing is expected and ICICI Bank with its new offering beats competition by a mile.

At the time of comparison the Spot SGD INR was 47.75 and below table shows how the 3 services which offer confirmed Rate transfer compared:

| Service | 3000 | 5000 | 10000 | 15000 | 20000 |

| Money2India | 47.18 | 47.35 | 47.48 | 47.52 | 47.54 |

| DBS Remit | 47.22 | 47.22 | 47.22 | 47.22 | 47.22 |

| SBI Remit | 47.3 | 47.3 | 47.3 |

As you can see for amounts 5000 SGD or more money2india had a substantially better rate than the competition and that happens because they have started charging 25SGD flat fee and reduced currency spreads. The rate money2india used was 47.66 and the results above are shows after taking the 25sgd fee and service charges into account.

Ofcourse the rates offered by money2india would change throughout the day but for transferring amounts greater than 5000 this would be my service of choice (the only other way to get a better rate is if you can find someone who wants SGD and would give you INR and deal at spot)

Couple of things to Note for Money2India transfer Service

1. Only allows upto 400,000 Rs equivalent to be transferred per day using the fixed rate service.

2. The rate is updated around 12:00 noon Singapore time

3. Has a internal daily limit i.e. if the amount they have allocated for a day has been reached customers are refused transfers

I would have expected that there be no limit on amounts being transferred. With these limits it feels that money2india wants to only have small transactions so that they can earn more transfer fee. The rate still is better than DBS but as a customer I find these limits back door way of giving less to customers.

Update: Money2India no longer has fixed fee transfer service and the rates offered are not as good as SBI or DBS. For comparison of rates please refer to the widget on right or at the bottom (when using a phone)